Bates Research | 05-04-23

MTMA Provides Uniform Framework for Licensing and Regulation of Money Transmitters

For those of you that read our article “Navigating the Money Transmitter Licensing Process,” you know that obtaining a license is a daunting task. State licensing requirements have been extremely difficult to navigate, with the details of the money transmitter license process varying from state to state. It is important to note that supervisory oversight also varies.

To alleviate significant pain points for applicants, state regulators have worked on initiatives to provide consistency and harmonization across the nonbanking industry through collaboration among state regulators, industry participants and the Conference of State Bank Supervisors (CSBS). The Money Transmission Modernization Act (MTMA) was created to modernize the money transmission industry by allowing for comprehensive standards and requirements that reduce regulatory burden and encourage innovation, and improved consumer protections that allow for less confusing rules across states. The MTMA was drafted in 2019 and was approved by CSBS in August 2021. It is intended to provide a uniform framework for states to regulate money transmitters.

Under the MTMA, all money transmitters must comply with licensing requirements and are subject to additional regulations intended to protect consumers. These requirements include providing adequate disclosures about fees, rates, and other important information; implementing anti-money laundering measures; creating customer complaint procedures; maintaining adequate capital reserves; and others, based on company size. Additionally, the MTMA contains an article addressing virtual currency, a regulatory topic not currently included in many states’ money transmission laws.

Three Key Benefits of MTMA

Consumer Protection

The MTMA would provide consumers with greater protection against fraudulent activities and enhance their confidence in the money transmission industry. The current regulatory framework often results in confusion for consumers and presents a barrier to entry for new money transmitters. By streamlining the licensing process, the MTMA would make it easier for legitimate money transmitters to enter the market, increasing competition and driving down costs for consumers.

Regulatory Oversight

Regulatory agencies would be armed with greater authority to oversee the money transmission industry, improving regulatory efficiency and reducing compliance costs for money transmitters. The law would encourage the use of a national licensing system for money transmitters, eliminating the need for state-by-state licensing, which is currently a heavy administrative burden for money transmitters. This would enable regulatory agencies to more effectively monitor the industry and take action against illicit activities, such as money laundering and terrorist financing.

Innovation

Innovation is the key to success for many financial institutions. The MTMA has the potential to drive innovation in the financial industry by creating a regulatory framework that encourages experimentation and new technologies. Certain provisions of the MTMA would provide a safe, controlled environment for various money transmitters to test new business models and innovations without being burdened by excessive regulation. This would pave the way for business models like faster payment systems and distributed ledger technologies to be tested and eventually implemented in the wider market, benefiting both consumers and money transmitters.

Legislative Landscape

State legislatures are generally responsible for drafting their own laws related to money transmission services. However, by following the MTMA as a template for their own individual laws, states can ensure that they provide better protection for their citizens who use these services.

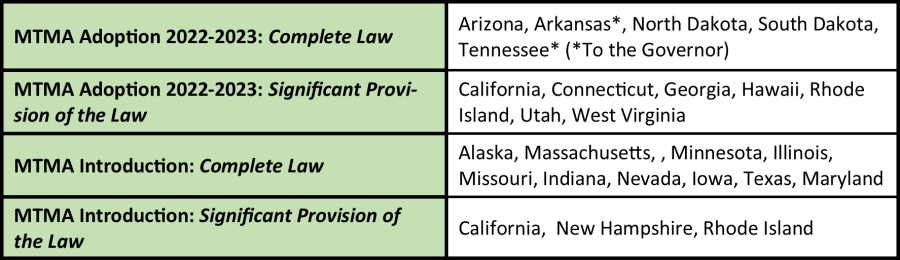

The CSBS has already seen success in having many states adopt versions of the model MTMA into their own individual laws. Currently, twenty states have either enacted or proposed legislation to implement the MTMA version developed by the CSBS. The chart below provides a breakdown of the current landscape.

Conclusion

The MTMA is a testament to the power of collaboration between the government and industry leaders. Widespread adoption would bring about significant improvements in regulating money transmitters, thereby safeguarding consumers from potential financial risks while fostering innovation.

About Bates:

Bates Group has been a trusted partner to our non-banking financial institutions and financial services clients and their counsel for over 40 years, delivering superior quality and results on a cost-effective basis. With a full professional staff and a roster of over 175 financial industry and regulatory compliance experts, Bates offers services in AML and compliance, regulatory enforcement and internal investigations, litigation consultation and testimony, forensic accounting, damages, and big data consulting.

Bates Group's MSB, FinTech and Cryptocurrency team provides a full suite of Bank Secrecy Act, Anti-Money Laundering and Office of Foreign Assets Control (BSA/AML/OFAC) compliance consulting services, state money transmitter licensing acquisition and maintenance support, independent reviews, and corporate compliance training.

For more information about Bates Group’s Money Transmitter Licensing and Maintenance services, please contact Bates today.

Contact