Bates Research | 03-21-23

Banking Update: Separating Fact from Speculation

by Greg A. Kyle, Director and Expert

In the aftermath of the collapse of three banking firms, Silvergate, Silicon Valley Bank and Signature Bank earlier in March, tensions in the banking sector continued over the past week with the shares of a number of regional banks including First Republic, PacWest Bancorp and Zions Bancorp under pressure. During the turmoil-filled week, several questions were raised about the strength of U.S. banks, whether regulators moved quickly enough, the role of venture capitalists, and if the failures were foreseeable.

We’ll start with the last question first.

Were the Banking Failures Foreseeable?

For many, nothing depicts a bank run like the classic film It’s a Wonderful Life. In the film, a bank in small-town middle America was faced with rumours over the safety of depositors’ money. In the movie, the citizens of Bedford Falls worriedly gathered at the doors of the Building & Loan early one morning waiting for it to open. They hoped to withdraw all their cash as rumours were spreading about the health of the institution.

After the seizures of Silicon Valley Bank and Signature Bank by their respective state regulators, there were rumours, internet chatter, and numerous people in the news who—after the fact—stated that the collapse of those two banks were clearly seen months prior. But was the sudden collapse-by-bank-run of Silicon Valley Bank and Signature Bank foreseeable? Despite what some have stated or speculated, the short answer is no.

As students of history, we’ve studied financial crises and bank failures from the Great Depression to today, and one fact that stands out is that, although bank runs have occurred in the past, the two precipitous bank runs that Silicon Valley Bank and Signature Bank faced were as unexpected as they were unprecedented.

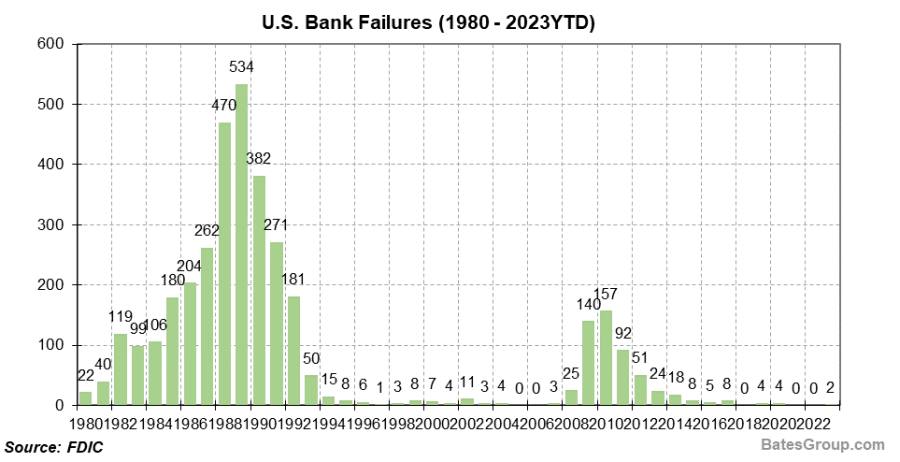

The early 1930s was a defining moment for the U.S. banking sector. In the wake of the stock market crash of 1929, the American public was nervous about any other potential financial disasters that could loom on the horizon. This made the period ripe for rumour and speculation and led to the 1930s being marked by a series of bank failures, with over 9,00 banks shuttering their doors between 1930 and 1933. In total, depositors lost over $7 billion in these failed banks—an estimated 20% of all bank deposits in the U.S. at that time. The dramatic impact these failures had on depositors led to the creation of the Federal Deposit Insurance Corporation (“FDIC”) in 1933.[i] Since then, bank failures and bank runs have been much less common.

During the savings and loan crisis of the 1980s to 1990s, nearly 3,000 financial institutions failed. There were sporadic runs during that period, but they were limited. The general view from the FDIC was that “deposit insurance virtually eliminate[d] the risk of bank runs,” with the only bank run of significance during this period being Continental Illinois National Bank and Trust Company in May 1984. At the time, Continental Illinois was the seventh largest bank in the U.S.

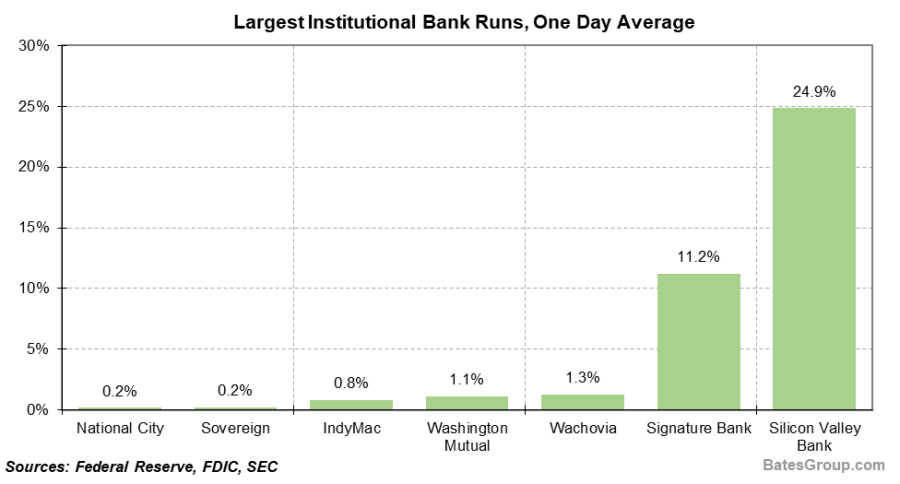

It wasn’t until the financial crisis in 2008 that bank failures rose sharply again. Between 2008 and 2010, over 300 banks failed, the majority due to lax credit requirements and significant losses on non-performing assets tied to the commercial and residential real estate markets. In 2008, several major institutions were hit with bank runs or large deposit outflows, the most notable being Washington Mutual at the height of the financial crisis. After the fall of Lehman Brothers in September 2008, WaMu experienced a bank run with $16.7 billion in deposit outflows over an eight day period. Following the collapse of Washington Mutual, Wachovia Bank also experienced significant deposit withdrawals on September 26, 2008, with outflows totaling $5.7 billion on that Tuesday.

Wachovia’s bank run on September 26 amounted to roughly 1.3% of total deposits that day. Washington Mutual’s bank run, while substantial, was spread over an eight-day period and averaged 1.1% of total deposits per day. There were a number of other bank runs in 2008, and the deposit outflows of those banks averaged between 0.2% and 0.8% of total deposits per day.

Fast forward to today. In contrast to the bank runs during the financial crisis, the bank runs on Silicon Valley Bank and Signature Bank were of a magnitude never previously experienced in U.S. history. According to California regulators, SVB experience $42 billion in deposit withdrawals on Thursday, March 9. With a deposit base of $169 billion, the bank experienced a precipitous bank run of 25% of its total deposits in a single day!

Similarly, Signature Bank also appears to have experienced a precipitous bank run. According to a CNBC article, in the wake of SVB’s sudden collapse, Signature Bank experienced $10 billion in deposit withdrawals in just a few hours late on Friday afternoon. With $89 billion in deposits, the late Friday bank run on March 10 amounted to 11% of total deposits. As can be seen in the chart below, the two bank runs experienced by SVB and Signature Bank that Thursday and Friday were, by far, the largest and swiftest runs in U.S. history.

Given the history of bank runs, it simply was not reasonable to believe, both in terms of magnitude and velocity, that the sudden precipitous bank runs on SVB and Signature Bank were foreseeable.

Did Venture Capitalists Play a Role?

What could explain the magnitude of the concentrated withdrawals? Rumours abounded that venture capital firms accelerated the collapse of Silicon Valley Bank by allegedly advising their portfolio companies to withdraw funds from SVB, while simultaneously withdrawing their own cash. Due to the concentrated nature of SVB’s depositor base (i.e., heavily concentrated in technology, health care and life sciences companies, with an early-stage focus), it’s plausible that a text or email blast, or other mass digital communication from a credible source (like venture capital firms) could produce an outsized reaction like the rapid and massive withdrawals that SVB experienced on March 9. Even without VC firms recommending to their portfolio companies to move money out of SVB, the concentrated focus on early-stage technology companies could also have impacted the deposit run-off rate (withdrawals). As discussed in our previous Banking Alert, in a rapidly rising interest rate environment, technology companies were experiencing a large-scale decrease in funding opportunities, causing them to burn through capital more quickly than in prior periods.

Quality of Assets – What is the Strength of the U.S. Banking Sector?

It’s worth remembering that plummeting share prices (often panic-driven) are one thing, but fundamentals are another. And, in terms of fundamentals, the banking sector is stronger today than in the past. As we wrote in our last Banking Alert, capital requirements have been strengthened, liquidity is stronger than in the past, and the quality of capital is better today than during the financial crisis.

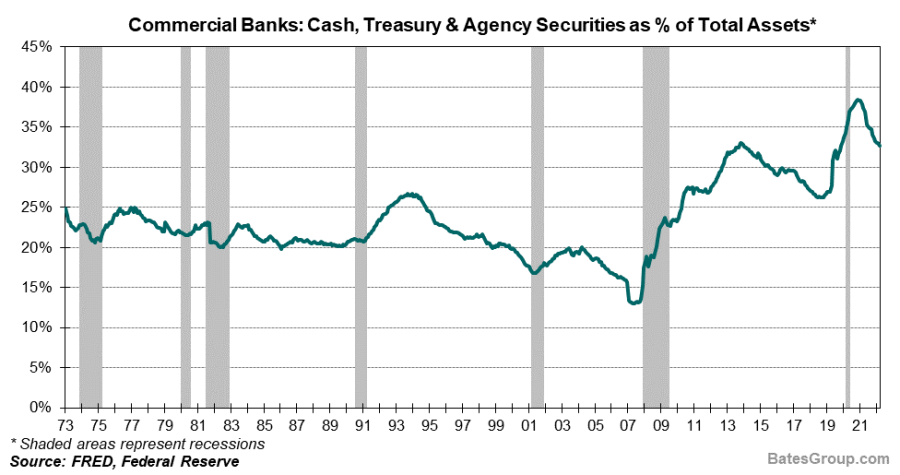

During the financial crisis, in aggregate only 10% of a bank’s assets were in government fixed income securities (U.S. Treasuries and Government Agency). Today, in contrast, banks have a much stronger asset base with nearly 20% of commercial banking assets in U.S. government securities. When cash is included, the share of high credit quality assets is at 33%, nearly three times what it was in early 2008.

And, when it comes to liquidity coverage using a strict measure such as cash held by banks as a percentage of total deposits, the banking sector is also much stronger today than during the financial crisis. In 2008 at the beginning of the financial crisis, cash held by commercial banks was less than 5% of total deposits. Today, in aggregate commercial bank cash holdings are 18% of total deposits. This does not include high quality liquid assets (“HQLA”) included in available-for-sale securities that banks hold today.

With the rapid rise in interest rates, those banks that did not adequately manage duration or asset-liability matching are seeing higher interest rate risk (and the associated price risk) exposure and unrealized losses. If those high credit quality securities do need to be sold, then unrealized losses can turn into realized losses. However, it’s worth bearing in mind that there is virtually zero credit risk associated with U.S. Treasury and Agency bonds, and these securities, despite changes in interest rates, will mature at par, thus reversing and eliminating the unrealized losses.

Did Regulators Move Quickly Enough, or Were Regulators Asleep at the Wheel?

Although it is too early to draw definitive conclusions, it appears that state regulators moved quickly and decisively to seize the two banks before further damage could be done. With Silicon Valley Bank, the California Department of Financial Protection took immediate possession and closed the bank after seeing the massive, unprecedented deposit outflows on Thursday. In Signature Bank’s case, New York Department of Financial Services seized the bank over the weekend. Although the specific reason was not given, it appears (at least from the CNBC article mentioned earlier) that it was due to significant deposit outflows late Friday, March 10. Each respective regulator acted within one business day to stem losses and minimize damage. In contrast, during the financial crisis, regulators waited days or even weeks as banks were experiencing runs on their deposits before acting.

There has also been some discussion that the roll-back of certain sections of the Dodd-Frank Act led to the collapse of SVB. At this point, that does not appear to be the case. The Dodd-Frank Act was passed in the aftermath of the financial crisis to protect consumers and taxpayers by tightening regulations for banks that were considered systemically important. Originally, the threshold of a systemically important institution was defined as one with total consolidated assets of $50 billion or greater. Banks above that threshold were required to conduct regular stress testing which, among other factors, take into account various economic scenarios and the impact of changing interest rates on a firm’s capital levels, asset prices and earnings. In 2018, the definition of a systemically important bank was changed to only include institutions with assets totaling over $250 billion. Silicon Valley Bank, with total assets of roughly $210 billion, fell under that threshold.

Would maintaining the threshold at $50 billion and requiring regular stress testing have prevented the failure of Silicon Valley Bank and Signature Bank? It appears unlikely. The sudden failure of these two banks were ultimately the result of precipitous one-day bank runs, and the stress tests detailed in the Dodd-Frank Act—and provided by the Office of the Comptroller of the Currency (“OCC”)—do not include bank run scenarios let alone single-day deposit outflows of the magnitude experienced by Silicon Valley Bank and Signature Bank. It should be noted that the Liquidity Coverage Ratio (“LCR”) implemented with Basel III is a requirement of Section 165 of the Dodd-Frank Act. However, in calculating LCR, deposit run-off rates ranging between 3% to 10% over a 30-day period are used. These deposit run-off rates would not be considered a bank run.

Going forward, protecting bank customers against massive bank runs will be an interesting policy debate. Gone are the days of depositors lining up around the block with deposit slips in hand waiting to withdraw their money. In the modern digital era when cash can flow quickly between institutions in a matter of minutes if not seconds, the question becomes how can banks protect themselves from sudden and extreme deposit outflows? What level of liquid assets (i.e., HQLA) relative to the deposit base should banks have on hand in order to meet potential large, single-day outflows? Should the definition of HQLA as detailed in Basel III and adopted by the Dodd-Frank Act be changed? Should the FDIC raise the level of deposit insurance from $250,000 to a higher level? Should regulators, or banks, be able to declare a banking holiday until concerns abate? What other measures can regulators enact to protect consumers and taxpayers from precipitous, massive bank runs in the future?

These are interesting policy and regulatory questions that are unlikely to be decided soon.

Other Thoughts

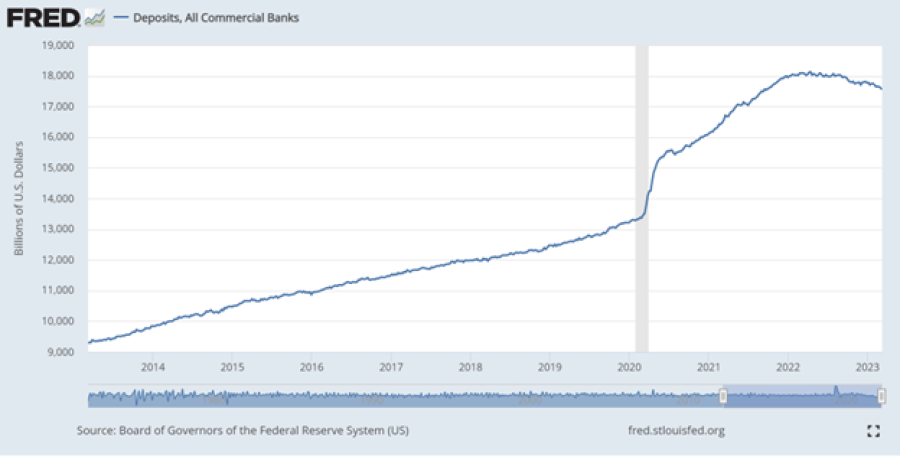

Did Silicon Valley Bank grow its assets too quickly? There has been some discussion that the rapid growth in SVB’s assets was a red flag of growing problems. However, it would be hard to argue that the rapid growth in assets was abnormal considering the massive increase in deposits that originated in early 2020 with the onset of COVID. Even today, deposit levels have remained very high (see chart below).

According to a report by the Federal Reserve, the ratio of deposits to GDP has remained above 75% since early 2020. That same report identified four trends impacting the sustained high ratio: (i) rapid draw down of commercial and industrial lines of credit; (ii) the Fed’s asset purchases; (iii) fiscal stimulus related to COVID; and (iv) a higher personal savings rate due to COVID. An interesting area for further investigation would be the extent to which the lack of loan demand (i.e., an absence of high demand for bank credit) during the pandemic period may have led to increased purchases of longer duration assets in order to earn a positive spread against a growing deposit base.

In terms of Silicon Valley Bank’s rapid asset growth, although total assets did grow from $71 billion at the end of 2019 to $211 billion at the end of 2022, U.S. government bonds as a percentage of total assets went from 36% in 2019 to over 50% in 2022. At the end of last year, 91% of the bank’s available-for-sale and held-to-maturity securities were in U.S. Treasuries and Agency bonds. It appears that the rapid growth in assets did not translate into a rapid growth in credit-riskier assets, rather a rapid growth in high-quality assets. Further, the bank was considered financially sound by California regulators prior to the precipitous bank run on March 9.

In an effort to restore investor and depositor confidence in First Republic Bank, a consortium of banking entities extended $30 billion in deposits in a major cash infusion to the bank. These included major financial institutions such as JPMorgan Chase, Bank of America, Wells Fargo, Goldman Sachs, Morgan Stanley and others. The importance of regional and small banks within the overall financial ecosystem was flagged explicitly as a rationale for the move. Larger financial institutions, those dubbed “too big to fail” after the crisis in 2008, experienced a spike in deposits amidst the bank turmoil, perhaps reflecting a belief that they would not be allowed to fail regardless of FDIC protection limits. A further $121 billion poured into money market funds, reflecting additional uncertainty around the banking sector, with nearly $100 billion coming from institutional sources and the remainder from retail investors. These inflows and outflows may have prompted the “vote of confidence” in First Republic by the larger entities.

And Credit Suisse? Internationally, Credit Suisse was offered 50 billion Swiss francs (approximately $54 billion) in liquidity facilities by the Swiss National Bank in an effort to improve its liquidity last Wednesday. The bank had experienced extensive challenges, including the withdrawal by depositors of 123 billion Swiss francs ($133 billion) in the fourth quarter of 2022. In February, the global bank also reported an annual net loss of $7.3 billion, the largest net loss since the global financial crisis. Its shares had declined by about 23% already this year.

Ultimately, UBS announced on Sunday that it would be acquiring Credit Suisse for around three billion Swiss francs, with Credit Suisse shareholders receiving one share in UBS for every 22.48 shares held in Credit Suisse. This value equates to approximately 0.76 Swiss francs per share, or about three billion Swiss francs in total. The Swiss National Bank participated by pledging up to 100 billion Swiss francs in loans to support the transaction, and the absorption of losses on certain assets above a preset threshold meant to reduce the risk to UBS from the acquisition. The move was generally applauded as a step towards additional stability in a rattled global banking system.

[i] The FDIC is a government agency that provides deposit insurance for depositors in FDIC insured banks. Originally the FDIC insured deposits up to $2,500, although that has increased over the years and today stands at $250,000.

About the Author:

Greg Kyle is a Bates Group director and expert based in New York. He uses his extensive background in the securities industry to consult and provide expert witness testimony on matters involving fixed income and credit market performance and analysis including mortgage- and asset-backed securities, equity market and security valuations, sector and asset allocation analysis, and fund risk disclosures. Mr. Kyle still actively analyzes the financial markets and publishes analyses of the economy and the capital markets.

Contact: